Audit reveals WCPS’ financial turmoil

A 2019 audit of Wayne County Public Schools’ finances shows several areas of interest, an independent auditor told the Wayne County Board of Education at a special called meeting Tuesday — everything from central office salaries and General Fund deficits to a $3 million transfer that no one is sure has been repaid.

The findings included:

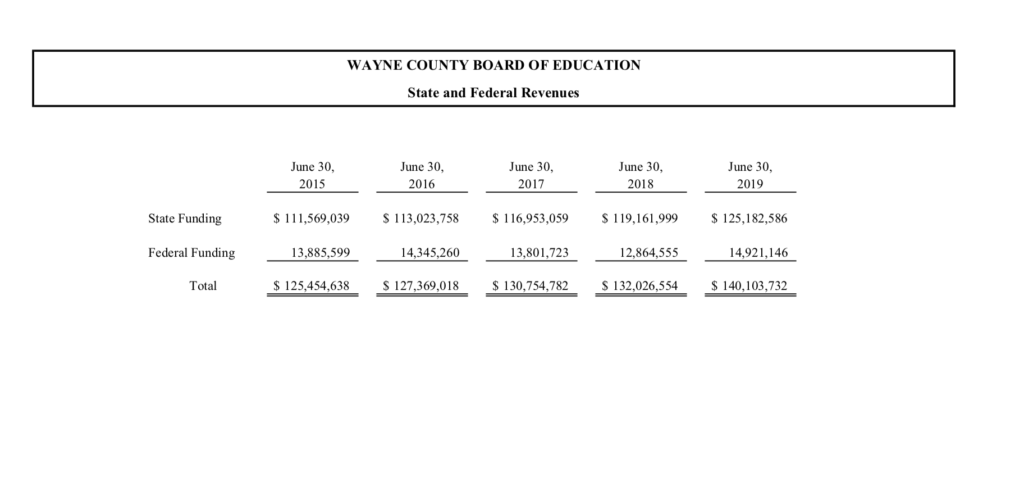

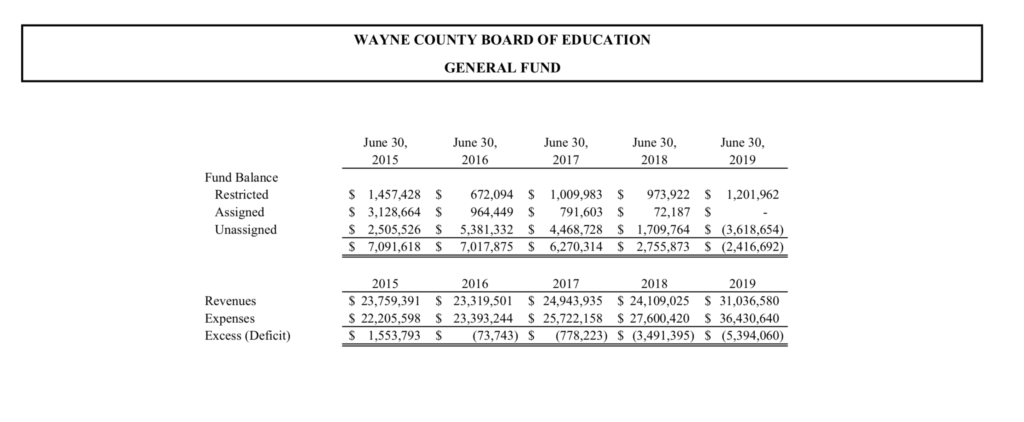

• A steep downward trend in the district’s fund balance — from $7.1 million in the black in 2015 to $2.4 million in the red in 2019.

• A steep upward trend in the difference between expenses vs. revenues over the same period — from $1,553,793 in the black in 2015 to about $5.4 million in the red in 2019.

• Steep increases in expenditures in several categories from 2016 to 2019, most notably spending on School Leadership, up 98 percent since 2016 — from $516,329 in 2016 to $535,525 in 2018, with a spike to $1,023,760 in 2019; a 300-percent increase in spending in Systemwide support and development; a 446-percent increase in Systemwide technology support spending from 2018 to 2019; and a 164-percent increase in Systemwide financial and human resources spending from 2016 — from $296,176 in 2016 to $792,150 in 2019.

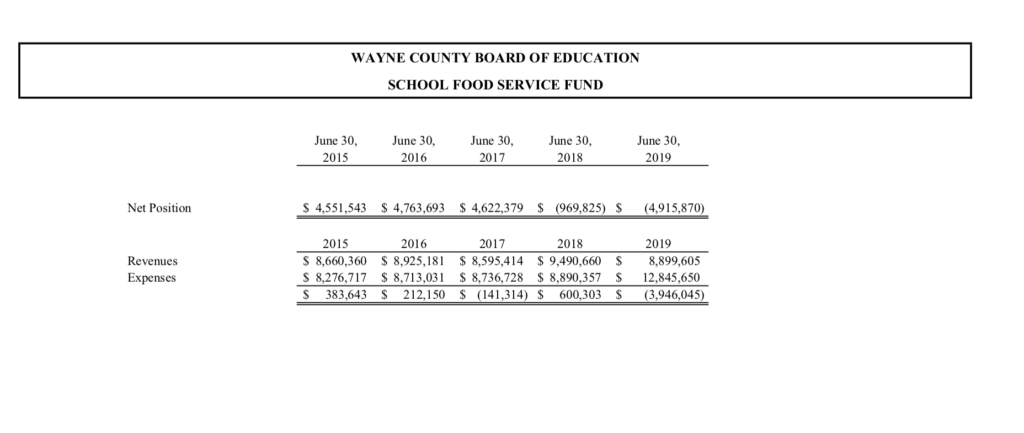

• A $3 million transfer “loan” made from the School Food Service Fund to the General Fund in 2019 and a finding of a negative balance of $3.9 million in that fund in 2019.

Diana Hardy, representing the audit firm Rives & Associates LLP, told the board that the auditors’ purpose is not to pass judgment on how the LEA (Local Education Agency) is operating financially, but to point out areas of concern that should be addressed by the board or management.

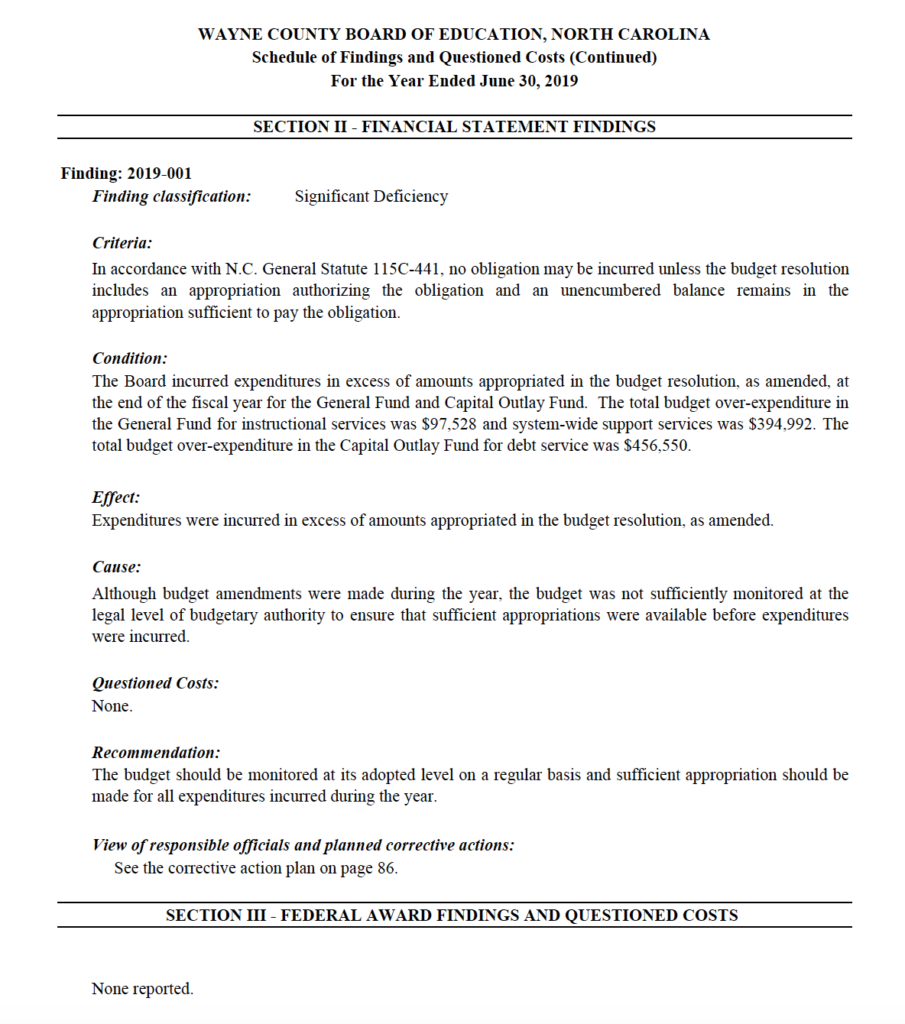

In the auditor’s report, the district was found to have incurred expenses in excess of amounts appropriated in the budget resolution in the General Fund and the Capital Outlay Fund.

The overspending was tagged at $97,528 for instructional services and $394,992 for systemwide support services. There was also an over-expenditure of $456,550 in the Capital Outlay Fund for debt service.

“Although budget amendments were made during the year, the budget was not sufficiently monitored at the legal level of budgetary authority to ensure that sufficient appropriations were available before expenditures were incurred,” the auditors concluded.

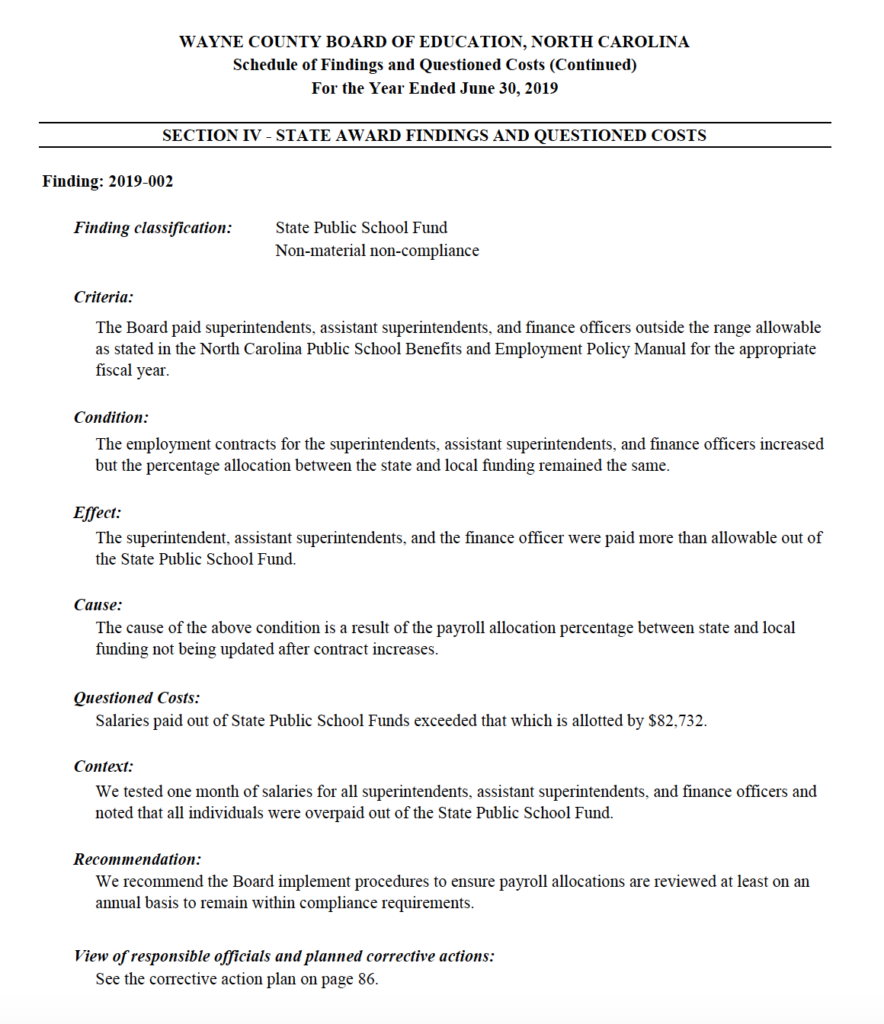

The report also concluded that the board “paid superintendents, assistant superintendents and finance officers outside the range allowable as stated in the North Carolina Public School Benefits and Employment Policy Manual for the appropriate fiscal year.”

That amount the district overpaid was $82,732.

The reason for the discrepancy was, the audit concluded, “payroll allocation percentage between state and local funding not being updated after contract increases.”

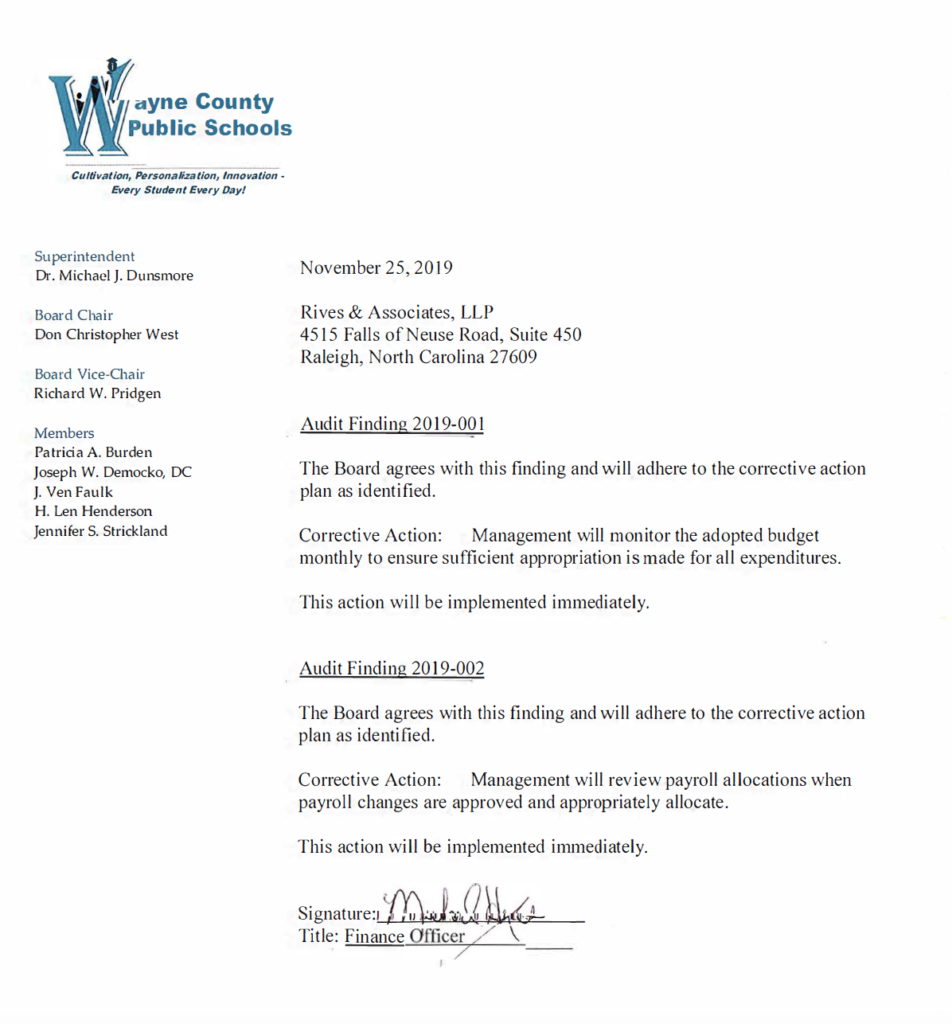

The audit recommended two courses of action — monitor the adopted budget monthly to ensure sufficient appropriation is made for all expenditures and that management will review payroll allocations when payroll changes are approved and appropriately allocate.

Finance officer Michael Hayes, who recently resigned his post, sent a letter to the audit firm in November 2019 certifying that the changes had been implemented.

Hardy also discussed two other recommendations — making sure reconciliation of accounts receivables is done in a timely manner and that manual journal entries are not made by those who would normally record the entries.

Also discussed during the meeting was a $3 million transfer made from the district’s School Food Service Fund.

The loan, which was made to the General Fund sometime during the 2019 school year, should have been repaid within a year, Hardy said in response to board members’ questions about the rules regarding such transfers.

She added that transfers of this nature are not uncommon, that the nature of the School Food Service Fund is that it generates revenue, which means it has a cash flow, unlike certain federal and state funding sources.

Money is “borrowed” from the fund, and then replaced when the other funds are received.

Hardy added that some of the multi-million-dollar deficit reported in the School Food Service Fund could also be attributed to an accounting change and retirement fund allotment rules.

The board questioned why the loan was made in the first place and if such a move had to be approved by the board.

Board members also asked if the loan has been repaid.

“I would have to look,” Superintendent Michael Dunsmore said.

Dunsmore said little during the audit presentation.

Most of the questioning came from Board Attorney Richard Schwartz.

Board Chairman Chris West said he has not seen the audit report, which was issued to the district, as required, in November.

Copies of the audit are traditionally sent to the superintendent and the finance officer.

Dunsmore indicated he had not seen the report and added that he did not know about the $3 million transfer.

“I was unaware of it,” he said.

Board members asked whether the dollars involved were federal money, which is monitored very strictly, and can incur penalties and fines if not used and accounted for properly.

The indication was that there were not federal funds involved.

“I am aware of loans that are made for cash flow issues, not for budget deficits,” Schwartz said.

After hearing the audit results, the board decided to postpone discussion of its 2020-21 budget, which includes a request for local funding from the county.

“We do not have a budget to discuss,” West said.

The board is expected to speak about the audit again during tonight’s continuation of its regular board meeting.

Hardy said Rives & Associates LLC included a handout with the audit presentation outlining the overspending in the General Fund and the accompanying percentage increases as a way for the board members to see the trend.

She did not offer an opinion on whether the increases were within acceptable or usual ranges.

“Is this a sign of the times or an indication of a concern,” West asked.

“The numbers that are presented are true and accurate,” she replied. “I think that chart is an eye-opener.”

Here are the pages of the audit that will help you understand the findings reported above:

This who wish to review the complete audit, can access it below:

A loaded discussion

Fighting for their lives

Goldsboro loses a giant

“I’m a flippin’ hurricane!”

Public Notices — March 8, 2026

Belting it out

Legendary

In her Nana’s image